25 April 2010

"There’s something missing from the current debate about GST, and that’s a tax alternative, one that targets the banks and financial speculators," says Vaughan Gunson, Bad Banks spokesperson.

"Instead of making food and other basics more expensive for grassroots people, New Zealand needs to introduce a Financial Transaction Tax, or Robin Hood Tax as it’s been named by a popular British campaign," says Gunson.

"A small percentage tax on financial transactions would net billions annually from the big banks and financial speculators, who shift enormous amounts of money around everyday," says Gunson. "We could then remove GST from our food and begin to phase out this horrible regressive tax altogether. This is the circuit breaker that the GST debate needs."

"Following the global financial implosion, and the role played by the banks and financial speculators, the time is right to introduce a tax which hits the most hated global purveyors of greed and exploitation. Yet the government is heading in the other direction, wanting to give tax breaks to these parasites, while hitting us with a GST increase," says Gunson.

Prime minister John Key wants to reward international financial speculators with tax breaks and other incentives, as part of his dream of turning New Zealand into a financial hub. The plan rests on enticing global investors to New Zealand with the promise of tax breaks. A recent IRD report entitled ‘Allowing a zero per cent tax rate for non-residents investing in a PIE [portfolio investment entity]’ reveals what's being considered. Under this proposal, overseas investors would be allowed to operate in this country and not pay New Zealand tax on their international investments.

"John Key would say that removing GST from food is too complicated - yet it’s not too difficult to change the tax laws to gift more profits to international fat cats?" asks Gunson. "Whose side are you on Mr Key? Hardworking grassroots people or the financial parasites?"

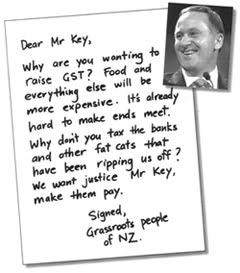

The Bad Banks campaign has drafted a letter to the prime minister on behalf of the grassroots people of New Zealand. It reads:

Dear Mr Key,

Why are you wanting to raise GST? Food and everything else will be more expensive. It's already hard to make ends meet. Why don't you tax the banks and other fat cats that have been ripping us off? We want justice Mr Key, make them pay.

Signed,

Grassroots people of NZ

With the letter the Bad Banks campaign is raising three "common sense" measures to curb banking power and protect grassroots people, which includes introducing a Robin Hood Tax. They are:

1. Stop forced mortgagee sales

Regulatory muscle used to stop banks turfing people out of their homes. A government body to oversee the re-negotiation of mortgages based on current market values and ability of the homeowner to pay.

2. Turn Kiwibank into a proper public bank

Offering 3% interest loans to first home buyers, zero-fee banking for people on modest incomes, and low interest loans to local bodies for sustainable eco-projects in the public good.

3. Introduce a Robin Hood Tax (also known as a Financial Transaction Tax)

A small percentage tax on financial transactions would net billions of dollars from banks and global financial speculators. GST could be phased out.

"We’re inviting people to sign-on electronically to our letter to prime minister John Key via the Bad Banks website www.badbanks.co.nz (or go directly to http://www.ipetitions.com/petition/badbanks/). We think a clear message needs to be sent to the government and John Key that it's the banks and other financial fats cats who must be made to pay," says Gunson.

The cartoon by KLARC accompanying this media release is available to be reproduced in print and web publications. For a bigger resolution image contact Vaughan at the email below.

For more comment, contact

Vaughan Gunson

Bad Banks spokesperson

svpl(at)xtra.co.nz

(09)433 8897

021-0415 082